Nov 29, 2023

The past year has been a particularly brutal one for the housing market. Buyers can’t afford to buy, sellers don’t want to sell, mortgage rates are at 20-year highs, and there are extremely few homes available for sale. The market, by most measures, appears to be frozen. Something has to give, right?

Now the question is if 2024 will be the year the housing market finally becomes unstuck. The answer is sort of.

Affordability is expected to improve a bit in the year ahead, according to the Realtor.com® 2024 forecast. At the very least, our economists don’t anticipate the market getting any more painful for buyers who have been grappling with the worst affordability challenges since the early 1980s.

“We’re not going to see a major breakthrough in the logjam that has been the housing market over the last year or so, but 2024 will be a baby step in the right direction,” says Realtor.com Chief Economist Danielle Hale. “It’s going to stop getting worse.”

While the market will stabilize, it’s expected to remain challenging. The Realtor.com annual forecast predicts home prices will remain high, mortgage rates won’t retreat as much as many have hoped, and move-in ready homes in desirable areas will remain scarce. However, the specifics will vary greatly by location.

“Everybody’s ready for the stalemate in housing to be over,” says Hale. “But the pieces aren’t in place for that to happen just yet.”

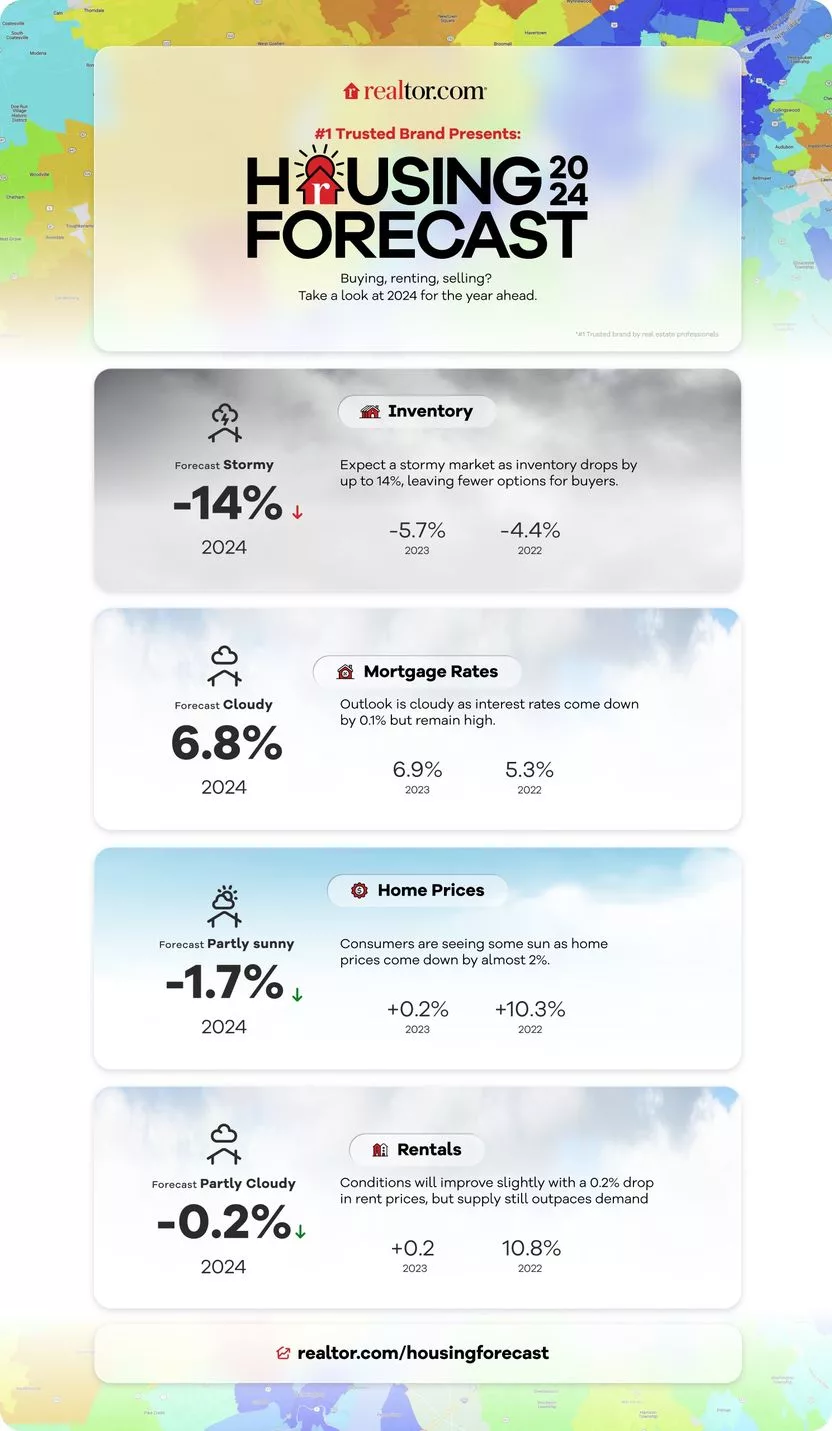

Home prices are expected to fall

Let’s get right to the good news: Home prices are expected to finally come down in 2024.

But don’t break out the Champagne—or panic—just yet. Prices are expected to tick down only about 1.7%. That’s not enough of a decline to offer most buyers meaningful financial relief. However, in most markets, they don’t need to be up all night worrying that if they don’t buy immediately it will get more expensive to do so.

The slight reduction will also give incomes a chance to catch up to these high prices. Typically, home prices rose about 6.5% a year from 2013 through 2019. During the COVID-19 pandemic, many buyers couldn’t save fast enough to keep up with increasing prices. The new year will effectively hit the pause button.

“It will be a bit of a break after what have been pretty relentless home price increases,” says Hale. “It’s going to be a big leap forward for buyers’ mental health. Some of the pressure and sense of urgency will start to let up.”

It’s also not a significant enough of a drop to be the reason why sellers don’t list their properties. Those who have owned their homes for a few years have likely accumulated substantial equity as home values spiked.

So even if prices dip, few homeowners will find themselves underwater on their mortgages like what happened during the Great Recession.

“It’s a really minor drop on top of what have been really major price gains over the last decade,” says Hale.

Mortgage rates will retreat a little

Higher mortgage rates have pummeled the housing market like an especially savage MMA fight.

In the past three years, rates have risen from the high 2% to the mid-7% range, according to Freddie Mac data for 30-year fixed-rate mortgages. That’s resulted in the typical mortgage payment more than doubling over the same period.

Unfortunately for buyers, our economists don’t anticipate rates coming back down to the lows seen during the pandemic.

The Realtor.com econ team anticipates rates will average about 6.8% for the year and fall to about 6.5% by year’s end. That’s about eight-tenths of a point lower than rates were last week (7.29%, according to Freddie Mac), but still much higher than the 4% historical average between 2013 and 2019.

“Small changes in rates can drive big changes in your monthly payments, especially when prices are high,” says Hale.

However, rates aren’t likely to fall enough to give the housing market the jolt that it so desperately needs.

Buyers making the national median income in 2024 are expected to spend an average of 34.9% of their earnings on their housing payments, going down to below 30% by year’s end. That’s better than this October, when buyers spent 39%, but still much higher than the 21% they spent between 2016 and 2019.

“Rising mortgage rates have priced a significant number of homebuyers out of the market because they’ve raised the cost of borrowing at a time when home prices are also close to record highs,” says Hale. “The double whammy is too much for many buyers.”

The housing shortage will get even worse

The largest pain point for many homebuyers in the year ahead (besides how much their bank accounts are squeezed) will be how few homes there are for sale to choose from. Even as it gets a little cheaper to purchase a home, buyers might not find anything they want.

It’s a vicious, self-perpetuating cycle. If homeowners don’t find anything they’re interested in buying, they are more likely to stay put. And that means there are fewer homes available for other buyers.

The number of existing homes for sale is expected to fall by 14% in 2024 compared with this year. (Existing homes exclude new construction.)

The problem is high mortgage rates are prompting many homeowners to stay put. About two-thirds of homeowners with mortgages have rates below 4%; more than 90% have rates that are less than 6%. There is little incentive for these folks to sell, especially when purchasing a new home at a higher rate will cost them so much more each month.

Those who list their homes and purchase new ones generally have to do so because their family situation changes, such as with a new baby or a divorce, or they’re relocating for a new job or retirement.

“We’re talking about moves of necessity for people,” says Hale.

The good news is builders are expected to keep putting up homes. Those numbers aren’t included in the housing inventory drop that Realtor.com predicts. Builders are anticipated to rev up construction about 0.4% over last year to just under a million new homes. And they’re likely to continue to offer incentives, such as mortgage rate buy-downs, to close deals.

“When buyers go shopping, they’re going to see more new homes,” says Hale.

Home sales will remain low

Since homeowners won’t be listing many properties and buyers are struggling to afford homes, sales are expected to remain low.

Realtor.com predicts the number of existing-home sales will increase by just 0.1%, to about 4.07 million homes sold in 2024.

While that might sound impressive during a housing shortage where prices and rates are elevated, it’s a significant tumble from the 5.28 million homes that were traditionally sold annually between 2013 and 2019. And it’s a dramatic drop from the 6.12 million sales in 2021 when the nation was still in the grips of the pandemic and mortgage rates were historically low.

Rents will get a little cheaper

As the housing market has priced many would-be buyers out, many have been forced to remain renters for longer. That’s left them vulnerable to landlords who have been steadily jacking up prices over the past few years.

However, after several years of meteoric price growth, the large price hikes are expected to end. Realtor.com predicts rents will go down 0.2% in 2024.

There will also be more rentals available for them to choose from, which should help to keep a lid on prices. Builders ramped up apartment construction over the past year.

“The fact that they’re not continuing to go up is going to be a welcome change,” says Hale. “We’ve had a near record level of apartment construction, and that’s helping to take the pressure off of rental prices.”

Source- https://www.realtor.com/news/trends/will-the-housing-market-roar-back-in-2024-our-fearless-predictions-for-the-year-ahead/