Nov 21, 2023

Successfully buying a home hinges on a bunch of numbers, from home prices to mortgage rates. And there’s a lesser-known figure that can make all the difference when realizing your homeownership dreams: your FICO score.

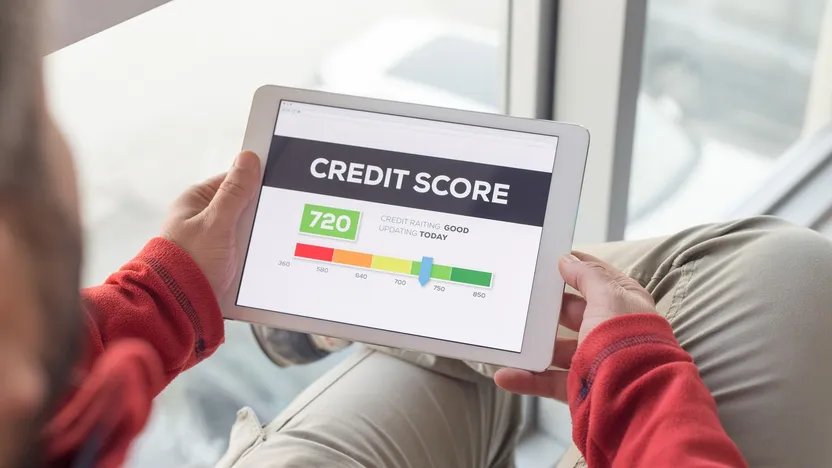

Whenever you want to make a big purchase, like a home, the lender will pull your FICO score, a three-digit number that represents your creditworthiness and is akin to a financial compass in the housing market. This number ranges from 300 to 850 and determines whether you’re approved for a loan, your interest rate, and your mortgage terms.

In essence, your FICO score is one of the many keys that unlock the doors of homeownership. To make sure you’re getting the best deal, you should understand how credit scores work before you apply for a loan.

What is a FICO credit score (and what does FICO stand for)?

While there are several types of credit scores, most lenders use the credit-scoring model developed by the Fair Isaac Corp.

This credit score, known as the FICO score, is a three-digit number ranging from 300 to 850. Lenders use the score to determine how risky it would be to loan you money.

For example, if your credit score is 420, you’re considered a very high-risk applicant and you may struggle to get approved or find good rates. If your credit score is 780, you’re considered a low-risk applicant and you’ll likely get the best rates and terms when you apply for a loan.

The three credit bureaus

FICO doesn’t collect information to determine your score. Instead, the information is collected by a credit bureau.

There are three main credit bureaus: Equifax, TransUnion, and Experian. Each credit bureau collects information about your financial habits and compiles the information into your credit history.

Your credit history stretches back seven years. In some cases, like with a bankruptcy, the history can go back to 10 years. Everything—from your application for a retail store card to whether you pay your bills on time each month—is reported on your credit history.

What goes into your score

To determine your FICO score, information from your credit reports is calculated using a formula. Certain actions are weighted more heavily than others:

- Payment history: 35%

- Debts owed: 30%

- Length of your credit history: 15%

- Types of credit you have: 10%

- Applications for credit: 10%

Figure out your credit score

If you’re considering making a large purchase, it is a good idea to pull your credit reports and credit scores several months before you apply for a loan. By law you’re entitled to a free copy of your credit report from each bureau once a year. You can request the reports through AnnualCreditReport.com.

You can order your credit scores for a small fee directly through the credit bureaus’ websites. Your credit scores are not included on your free credit reports.

Source- https://www.realtor.com/advice/finance/fico-credit-scores-explained/